What to Do When a Sibling Refuses to Pay for an Aging Parent’s Expenses

When an elderly parent begins to need financial support, families often assume everyone will contribute in some way. But in reality, situations are rarely that simple. One son may be covering medical bills, a daughter may be managing daily expenses, while another sibling avoids contributing altogether.

When this happens, frustration builds quickly, not just because of the money, but because of the feeling that responsibility is not being shared fairly.

If you are dealing with this situation, whether you are a brother paying more than expected, a sister managing expenses across households, or siblings trying to coordinate finances between different bank accounts, you are not alone. Many families struggle with this exact issue. The key is not to avoid the problem, but to handle it with structure, clarity, and a system that makes contributions visible and fair.

If you are just starting this process, it helps to first understand the basics of SupportPay-style approaches to managing finances between siblings. This creates a foundation before addressing conflict.

Why a Sibling May Refuse to Contribute

Before reacting emotionally, it is important to understand why a sibling may not be contributing. In many cases, the issue is not a simple refusal, but rather it is a lack of clarity, communication, or structure.

Lack of Visibility Into Costs

A sibling who is not directly involved in caregiving often does not see the full financial picture. Medical bills, groceries, transportation, home care, and unexpected expenses add up quickly. Without a clear breakdown, they may underestimate how much support is actually needed.

Financial Limitations

Not all siblings are in the same financial position. A brother supporting his own household or a daughter managing her own family expenses may genuinely struggle to contribute. However, when this is not communicated clearly, it can appear as unwillingness rather than limitation.

Avoidance of Conflict

Money conversations are uncomfortable. Some siblings avoid them entirely, hoping the situation will resolve itself. Unfortunately, silence often creates more tension, especially when one sibling feels they are carrying most of the burden.

Different Views of Fairness

One sibling may believe that time spent caregiving counts as a contribution, while another believes financial input is what matters most. Without a shared definition of fairness, disagreements are inevitable.

Let’s explore the various options you can use in case siblings are refusing to pay:

Step 1: Get a Clear Picture of All Expenses

Before asking any sibling to contribute, you need complete clarity on the financial situation. Conversations based on assumptions rarely lead to agreement. Conversations based on numbers are far more productive.

Start by documenting all caregiving-related expenses, including:

- Medical bills, prescriptions, and insurance gaps

- In-home care services or assisted living costs

- Groceries, utilities, and daily living expenses

- Transportation and travel for appointments

- Home modifications and safety upgrades

- Legal or administrative costs

This step is critical because it shifts the conversation from emotion to evidence. Instead of saying, “I feel like I’m paying more,” you can say, “Here is exactly what has been spent and what is needed moving forward.”

For a deeper understanding of how families typically break down these costs, refer to guides for siblings on the cost splitting of caring for elderly parents. This helps anchor your discussion in practical examples rather than personal opinion.

Step 2: Define What “Fair” Means (Not Just Equal)

One of the biggest mistakes families make is assuming that fairness means equal contributions. In reality, equality is not always fair.

A daughter who lives close to a parent may spend hours each week managing appointments, medications, and daily needs. A son living in another city may not be able to provide that level of hands-on support, but may be in a better position to contribute financially. Another sibling may have limited income but can assist with administrative tasks or coordination.

Fairness comes from balancing these contributions and not forcing them into a rigid 50/50 split.

Families often use one of the following approaches:

- Equal contributions when financial situations are similar

- Income-based contributions when there are large income differences

- Hybrid contributions where time and money are both considered

The goal is to create a system that reflects real-life circumstances across siblings, households, and financial situations. Once everyone understands what “fair” actually looks like, the conversation becomes far more constructive.

Step 3: Ask for Specific Financial Contributions

One of the most common reasons siblings do not contribute is that the request is too vague. Saying “we need help” or “you should contribute more” does not give anyone a clear action to take.

Instead, be specific. Define:

- The exact amount needed

- What the contribution is for

- How often it is expected

- How payments will be made

For example, instead of asking generally for help, you might say:

“Can you contribute $250 per month toward Mom’s medical and caregiving expenses?”

This level of clarity removes confusion and makes it easier for siblings to respond. It also signals that the request is based on real numbers, not assumptions.

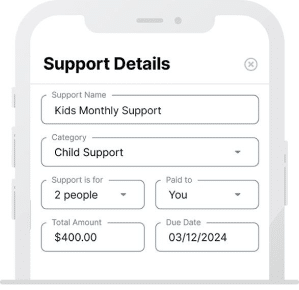

Step 4: Use a System to Track Contributions Across Households and Bank Accounts

Once expectations are clear, the next challenge is execution. Most families fail here not because they disagree, but because they lack a system.

When siblings live in different cities, manage separate households, and use different bank accounts, informal tracking quickly breaks down. One son may pay for medical bills, a daughter may handle groceries, and another sibling may contribute occasionally. Without a centralized system, it becomes impossible to see who is actually contributing and how much.

To avoid confusion, set up a shared system that:

- Tracks every expense in real time

- Shows who paid for what

- Records contributions from each sibling

- Works across multiple households and bank accounts

This is where structured financial coordination becomes critical. Families that succeed in these situations rely on systems that give everyone visibility, regardless of location. If you need a practical framework, you can explore how to manage money across households and bank accounts using structured tools and methods.

When every sibling can see the same financial picture, assumptions disappear, and decisions become easier.

Step 5: Put the Agreement in Writing

Verbal agreements rarely hold up under stress. Even when everyone agrees initially, misunderstandings can arise later.

To avoid this, document the arrangement clearly. This does not need to be a formal legal contract, but it should include:

- Each sibling’s financial contribution

- How expenses will be tracked

- Payment timelines

- Reimbursement rules

- A schedule for reviewing the arrangement

Having this written down creates accountability. It ensures that every sibling understands their role and prevents disagreements about what was originally decided.

What If Your Sibling Still Refuses to Pay?

Even after clear discussions and structured systems, some siblings may still refuse to contribute. At this point, the focus should shift from persuasion to management.

Keep Tracking Everything

Continue documenting all expenses and contributions. Even if one sibling is not participating, maintaining accurate records protects fairness and transparency for everyone else.

Revisit the Conversation With Data

Instead of approaching the issue emotionally, return to the conversation with facts. Show the total costs, the contributions made by each sibling, and the gap that remains. This approach is far more effective than repeating the same request without evidence.

Bring in a Neutral Third Party

If direct conversations are not working, consider involving:

- A family mediator

- A financial planner experienced in eldercare

- An elder law advisor

A neutral perspective can help shift the conversation from personal conflict to practical resolution. This is especially important in situations where caregiving responsibilities are becoming overwhelming, as explored in discussions around caregiving turning into a second job.

Accept Limits and Adjust the Plan

In some cases, a sibling may not contribute either due to financial constraints or personal choice. While this is not ideal, the focus should then shift to creating a workable plan among the contributing siblings rather than allowing the situation to stall entirely.

Common Mistakes to Avoid

- Not documenting expenses from the beginning

- Assuming siblings understand the full financial picture

- Mixing personal and caregiving expenses

- Using emotional arguments instead of financial clarity

- Avoiding difficult conversations until resentment builds

- Failing to create a system that works across households and bank accounts

Avoiding these mistakes can significantly reduce conflict and make financial coordination more manageable.

FAQs

1. What should I do if my sibling refuses to pay for our parents’ care?

If a sibling refuses to contribute, start by documenting all caregiving expenses and clearly showing the total cost. Then request a specific financial contribution rather than general help. If they still refuse, continue tracking expenses across households and bank accounts and consider involving a mediator or financial advisor to support the discussion.

2. Is it legally required for siblings to pay for a parent’s expenses?

In most cases, siblings are not legally required to contribute unless specific laws apply in certain regions (such as filial responsibility laws). However, financial responsibility is usually handled within the family through agreement, transparency, and shared planning rather than legal enforcement.

3. How can siblings fairly split elderly parent expenses?

Siblings can split costs equally, proportionally based on income, or through a hybrid model where some contribute money and others contribute time. The most important factor is agreeing on a system that reflects each sibling’s situation and tracking all contributions clearly.

4. What is the best way to track shared expenses between siblings?

The best approach is to use a shared system that records every expense, contribution, and reimbursement in one place. This ensures transparency across households and bank accounts and helps prevent misunderstandings about who paid what.

5. What if one sibling contributes time but not money?

Time is a valuable contribution in caregiving. A sibling who provides hands-on support, such as managing appointments or daily care, may contribute less financially. Families should recognize this balance and adjust financial contributions to reflect both time and money fairly.

Final Thoughts

When a sibling refuses to contribute, the situation can feel unfair and frustrating. But without structure, it can quickly become unmanageable. The solution is not to force agreement—it is to create clarity.

Families that handle these situations well focus on:

- Clear financial visibility

- Defined contribution systems

- Structured tracking across households and bank accounts

- Ongoing communication

When every sibling can see the same financial reality, decisions become less emotional and more practical.

Tools like SupportPay help families track shared caregiving expenses, manage contributions across different households and bank accounts, and maintain transparency over time. With the right system in place, even difficult situations can be handled in a way that protects both your parent’s care and your family relationships.