It usually starts with something small.

A grocery run. A prescription pickup. A co-pay that needs to be covered “just this once.” Then a new recurring cost appears, and another, and another. Before you know it, you’ve become the default coordinator for aging parents expenses—not only paying, but tracking, explaining, reminding, and smoothing over the awkward parts no one wants to say out loud.

That’s the part people rarely talk about: it’s not the expenses alone. It’s the coordination. The constant mental tabs you keep open. The emotional weight of needing to be both helpful and “fair.” The fear that one wrong text message could turn into a family rift.

And if you’re thinking, “Why does this feel so hard?”—it’s because most families are trying to manage shared responsibilities with individual tools.

Why It Feels Messy Even When Everyone Has Good Intentions

Most people say they currently track and split costs using spreadsheets/online documents, email chains, text messages, etc.

That’s not a system. That’s a patchwork.

It works for a week, maybe a month—until one receipt goes missing, one person forgets to respond, or one sibling interprets “I’ll cover it” as “I guess you’ve got this.”

So the real conflict isn’t always about money. It’s about ambiguity.

- What counts as “family” spending vs. personal choice?

- Who is responsible for what?

- What happens when someone can’t contribute the same amount?

- How do you handle reimbursement without turning relationships into invoices?

When “Siblings Not Contributing” Becomes The Third Person in The Room

Most families don’t sit down and decide, “Let’s create resentment.”

Resentment happens when contribution becomes invisible.

Maybe one sibling lives closer and does the errands, so it feels “natural” they handle payments. Maybe another sibling contributes emotionally but not financially. Maybe someone is struggling, avoiding the conversation, or quietly assuming the person who’s paying is “fine.”

Over time, siblings not contributing stops being a one-off frustration and becomes the story you tell yourself:

- “They always disappear when it’s time to pay.”

- “I don’t want to ask again.”

- “It’s easier to just do it.”

That’s how caregiving turns into a private burden—carried by the person least willing to create conflict.

A helpful reframe: most families don’t need perfect equality. They need shared reality.

Because without shared reality, every expense looks suspicious, every reminder sounds accusatory, and every silence feels like disrespect.

The Quiet Trap: Shared Expenses That Don’t Feel “Shared”

Once you’re coordinating shared expenses, you end up managing two ledgers:

- The financial ledger (who paid what)

- The emotional ledger (who shows up, who doesn’t, who notices, who appreciates)

The emotional ledger is the one that drives blowups.

That’s why a practical shift can change everything: stop trying to “win fairness” through conversation, and start building clarity through structure.

Clarity looks like:

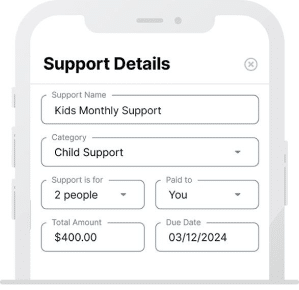

- a single source of truth for what was paid and why

- receipts attached to context

- a predictable cadence for settling up

- agreed categories (medical, home support, transportation, etc.)

Not because you want to be controlling—but because you want to stay connected.

Lending Money to Family: Where “Helping” Turns Into Awkwardness

If there’s one scenario that tests relationships faster than reimbursements, it’s lending money to family.

It often starts lovingly: “Don’t worry about it, just pay me back when you can.”

But unclear terms create unclear expectations—and unclear expectations create tension.

The loan itself isn’t always the problem. The uncertainty is.

A useful rule of thumb (that protects relationships):

- If you need it back, make it specific (amount, timeline, how repayment happens).

- If you can’t risk resentment, treat it as support and be honest with yourself about that.

How Financial Burnout Sneaks Up On The “Responsible One”

People don’t usually declare, “I’m in financial burnout.”

They say things like:

- “I’m tired of being the one who remembers everything.”

- “I can’t keep chasing people.”

- “I’m doing receipts at midnight.”

- “I feel guilty if I don’t pay, but resentful when I do.”

Financial coordination is rarely a “task.” It becomes an always-on role.

What Helps Most: A Simple Operating Agreement For Family Money

You don’t need a perfect plan. You need a plan you can stick to.

Here’s what a “family finance operating agreement” can look like—written in plain language, not legal language:

- Define what counts

- Which expenses are shared?

- Which expenses require a heads-up before purchase?

- Choose a split method

- Equal split, income-based split, or role-based split (e.g., one person does logistics, another contributes more financially)

- Set a cadence

- Weekly, biweekly, monthly—whatever reduces “surprise asks” and end-of-month stress

- Make receipts easy

- One place to store them, with a short note so nobody has to reconstruct context later

- Decide how disagreements work

- A simple rule like: “If someone disputes within 7 days, we talk. If not, we settle.”

This is the difference between “I’m constantly negotiating” and “we have a shared process.”

It’s not just a budgeting problem. Majority of people will have to coordinate money with someone at some point; it’s not niche, it’s normal life.

Where SupportPay Fits In

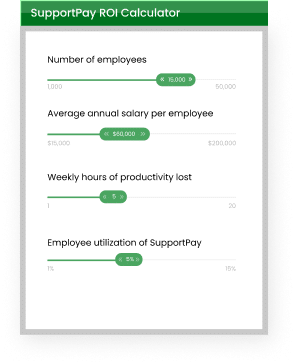

Some families build this operating agreement with spreadsheets and discipline. Others use a shared system designed for coordinating money across households.

But regardless of the tool, the goal is the same:

- reduce ambiguity

- reduce chasing

- reduce “who paid what?” fights

- protect relationships before the tension hardens into something permanent

A Small Next Step That Can Change The Next 30 Days

If you’re in the thick of it, try this:

Pick one category (meds, groceries, transportation, home help). Track it for 30 days with receipts and notes. At the end of the month, settle once—with a clear summary.

It’s not about being strict. It’s about being sustainable.

Because the real win isn’t a perfectly balanced spreadsheet.

It’s getting your time back, lowering the temperature in family conversations, and stepping out of financial burnout before it becomes your new normal.