Written By: John Reilly

Even if you have a co-parenting arrangement, the child or children will spend more time with one parent than the other. The law states that the non-custodial has to pay child support to the parent who has primary custody.

This is because the courts want a couple’s divorce to have the lowest possible negative impact on the children. So, if they were accustomed to a certain standard of living, this should be maintained as far as possible. This means that even a non-custodial parent who earns less than the custodial parent is still financially responsible for their children.

Despite the phrase ‘deadbeat’ being thrown around to describe parents who fail to pay child support, most times, parents want to provide for their children, but circumstances prevent them from doing so. A parent may lose their job, become ill, or have an accident preventing them from working, or, as the cost of living rises, they may simply not earn enough to support their children.

While child support is a basic need to maintain your children, billions of dollars are owed in back child support payments that have been court-ordered. Even though parents who owe money in child support are not withholding payment deliberately, the consequences of not paying are severe. Since child support is court-ordered, not paying is seen as being in contempt of court. Some of the consequences include:

● Your wages may be garnished. If you don’t pay child support, your co-parent can have your wages garnished. Your employer will be instructed to withhold a portion of your salary and use it to pay off the amount you owe in child support. The court will either garnish the total court-ordered amount of child support or up to 65% of your disposable income that the court determines.

● Your tax return can be seized. Your tax return can be withheld and used to pay your outstanding child support like your paycheck.

● A lien may be placed against your assets. Liens can be placed against assets like real estate or vehicles. The parent will have to pay the amount they owe before the lien expires. If the lien expires and they have still not made the payments, the assets that the lien was placed against can be seized. You will also be unable to sell this property until your debt is repaid.

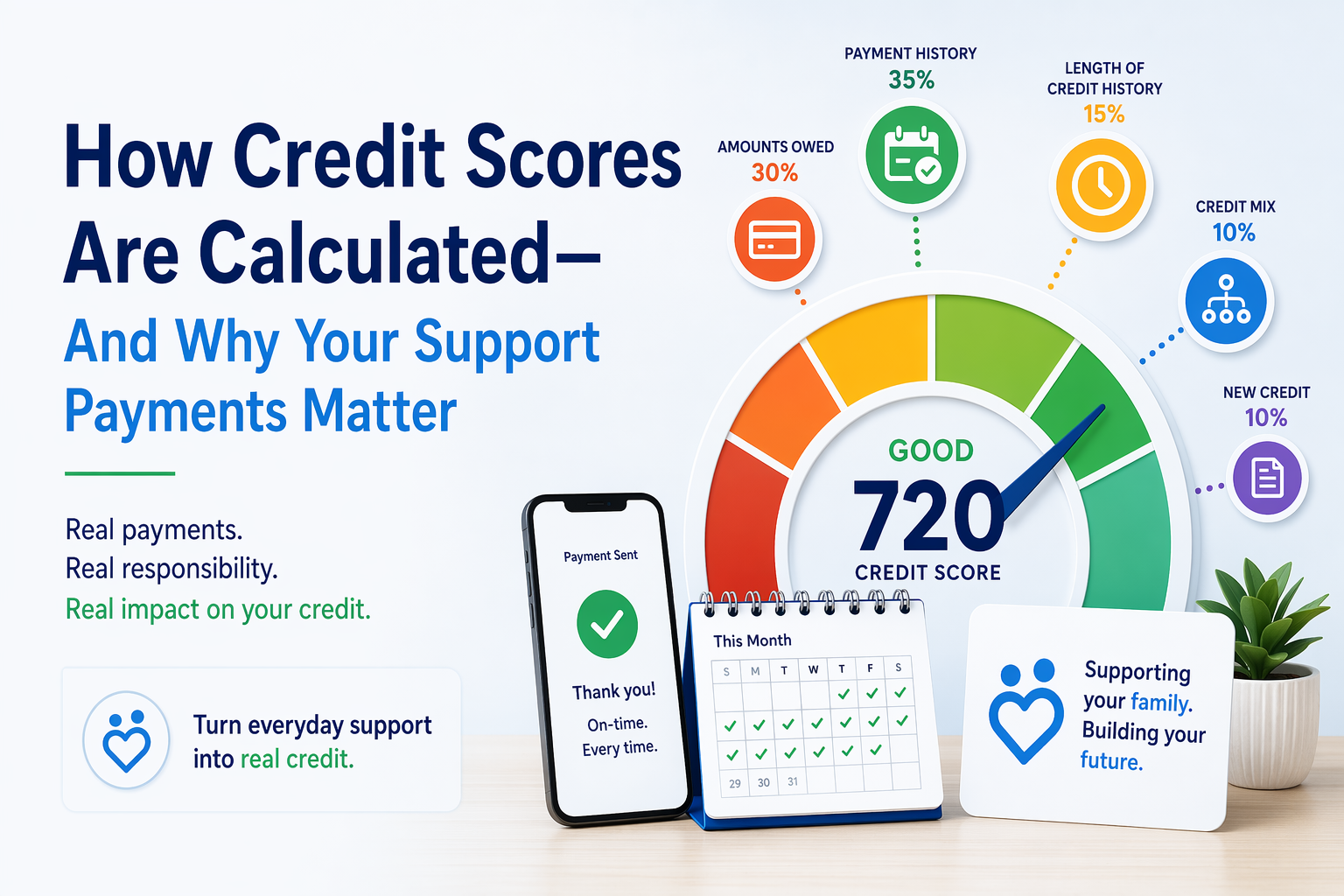

● Your credit score may drop. Non-payment of child support is considered debt, and child support agencies can report this debt to the credit bureau. Not paying your debt will hurt your credit rating, making it difficult for you to borrow money.

● Your driver’s license can be suspended. According to legislation in all states, failure to pay child support can result in losing your driver’s license. You could also lose professional or occupational licenses like a license issued by a medical board or recreational licenses like fishing, depending on the state you live in.

● Incarceration. Since not paying child support is being in contempt of court, you could face jail time for non-payment. This is usually in cases where the parent has missed many payments and has not attempted to pay.

Can’t Pay Child Support?

The worst thing to do is take a reactive approach, waiting to be contacted or hoping the problem will disappear. Instead, you must be proactive as this show your co-parent and the court that you want to support your child and will do what you can to get help.

As soon as you know you won’t be able to pay child support, do the following:

Let Your Co-Parent Know

The first step is to let your co-parent know about your financial situation since your lack of payment will affect them and your child. Your co-parent likely relies on child support to pay for school fees, clothes, medical insurance, and other expenses for your children.

Letting them know allows them to plan their budget, so your children are minimally affected. Let the custodial parent know if you can’t pay the total amount or can only manage to pay a portion of the court-ordered amount.

While this is not a legal requirement, it is in your child’s best interests to do so. Being transparent may also prevent your co-parent from pursuing legal action against you.

Since child support is court-ordered, your co-parent has no authority to release you of your financial obligations towards your child. Still, you may be able to work out an arrangement with your co-parent if your financial issues are only short-term.

For example, if you’re between jobs or need to take unpaid time off for a month or two but will return to work and be able to pay again. In this case, you may arrange with the custodial parent that you will not pay child support for two months or pay a reduced amount and then pay extra in the months after that to make up for the amount you owe.

Inform the Court

It is absolutely imperative that you get in touch with the Child Support Office or Court in the state your child support order was issued and let them know about your financial situation, especially if your financial difficulty seems to be long-term. You should let the court know even if the custodial parent has agreed to accept a reduced amount.

The judge will likely be sympathetic to your plight if you’ve reached out sooner rather than when you’re thousands of dollars in arrears.

If you are unsure when you will b able to pay the amount that’s been court-ordered, you can request a modification of the amount you pay, which a judge can only grant. You will need to explain why you can’t pay the original amount to support your case.

Regardless of Your Financial Situation, Your Child Needs to Have Their Expenses Met

You may be successful in getting your child support order modified to an amount you can afford, but if your co-parent can’t make up the amount you were paying, it may harm your children. The costs associated with raising children increases along with the cost of living. If all your child’s financial needs are not met, you may need to find other ways to provide.

One way to financially support your children is to look for fast personal loans. A loan can be helpful for specific times of the year when your financial obligations towards your children increase. This can be at the beginning of the school year when you must pay for back-to-school necessities or during the holidays. It can also be helpful when you are not working and without an income, like when you’re between jobs or on unpaid sick leave. In these cases, you know you will get back to work, so you will be able to repay the loan.

You may think you’d rather pay a lower amount in child support or not pay child support at all since, when you take out a personal loan, you will have to repay it plus interest. Still, a loan allows you to provide for your children, so you can take comfort in knowing that even though you will have to repay the loan, your children’s lives won’t be negatively impacted.

An option is to apply for a personal loan with reasonably good terms and a low-interest rate from traditional lenders like banks, provided you’ve got good credit. This will give you sufficient time to pay back the loan comfortably.

If your credit score is bad, you may struggle to secure a loan from a bank, but other personal loans are available that don’t have terrible terms, like personal loans from a credit union. It would be helpful to research the best options available to suit your needs, but ensure you’re familiar with the terms and confident you can repay your debt before committing to another financial obligation.

About the Author:

John Reilly is a freelance content writer during the day and a bookworm at night with an extensive background in finance and investments. He also has a business degree and aims to educate people about financial literacy through his articles.

References:

● Debt: Child Support Payment Financial Help

● Jacksonwhitelaw: How Does Child Support Work if Custodial Parent Makes More Money?

● Verywellfamily: When You Can’t Afford Child Support Payments