Introduction: Financial Stability Starts with a Plan

Every family wants financial security, but many struggle with unexpected expenses, debt and economic uncertainty. Whether you’re a two-parent household, single parent, blended family or co-parents managing finances separately, having a clear financial plan is the key to long-term stability and peace of mind.

Without a plan, you can:

❌ Overspend and accumulate debt

❌ Struggle with unexpected expenses

❌ Be unprepared for emergencies or significant life events

❌ Experience financial conflicts, especially in co-parenting situations

But with a well-structured financial plan, families can:

✔ Set financial goals and work towards them

✔ Manage shared expenses without conflict

✔ Save for significant milestones like college, homeownership or retirement

✔ Reduce stress by knowing exactly where your money is going

In this guide, we’ll cover why financial planning is essential for families and a step-by-step approach to creating a plan that works for your situation.

1. Why Every Family Needs a Financial Plan

Many people think financial planning is only for the wealthy or those with complex investments—but that’s not true.

A solid financial plan benefits all families regardless of income level because it provides:

✔ A Clear Roadmap for the Future

Just like a GPS helps you reach a destination, a financial plan guides your family to financial security. Without one, you’re just guessing where your money should go.

✔ Protection Against Emergencies

Life is unpredictable—medical bills, job loss or car repairs can throw finances into chaos. A financial plan ensures you’re prepared for the unexpected.

✔ Reduced Financial Conflict

Money disagreements are one of the leading causes of stress in relationships—especially for co-parents. Precise financial planning reduces tension and keeps finances fair and transparent.

✔ A Stronger Future for Your Children

Whether it’s saving for education, extracurricular activities or healthcare, a financial plan ensures your children’s needs are met without financial strain.

💡 Bottom Line: A financial plan isn’t a luxury—it’s a necessity. And the best time to start? Now.

2. How to Create a Family Financial Plan in 5 Steps

Step 1: Assess Your Current Financial SituationBefore you start creating a plan you need a clear picture of your family’s financial health.

✔ List all income (salaries, child support, government benefits, side gigs)

✔ Track all monthly expenses (rent/mortgage, utilities, groceries, childcare, insurance)

✔ Identify outstanding debts (credit cards, car loans, student loans)

💡 Use budgeting apps or a simple spreadsheet to track this information. The goal is to see exactly where your money is going.

Step 2: Set Short- & Long-Term Financial Goals

Every family’s goals are different, but they typically fall into two categories:

✔ Short-term goals (1-5 years) – Paying off debt, building an emergency fund, planning a vacation or saving for a new car.

✔ Long-term goals (5+ years) – Buying a home, saving for college, investing for retirement.

💡 Pro Tip: Make your goals SMART—Specific, Measurable, Achievable, Relevant, and Time-bound. Instead of saying, “I want to save money,” try “I want to save $10,000 for a down payment in 3 years.”

Step 3: Create a Realistic Budget

A budget ensures your money is going towards the things that matter most.

A great rule of thumb is the 50/30/20 rule: ✔ 50% on essentials (housing, food, transportation, childcare)

✔ 30% on wants (entertainment, hobbies, vacations)

✔ 20% on savings & debt repayment (emergency fund, retirement, paying off loans)

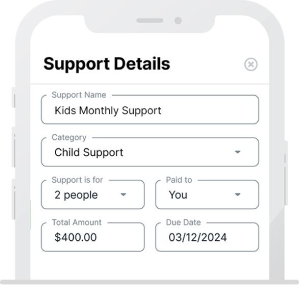

💡 If you’re co-parenting, use a tool like SupportPay to track shared expenses. This ensures transparency and prevents arguments about who owes what.

Step 4: Build an Emergency Fund

Experts recommend saving 3-6 months’ worth of expenses to cover unexpected financial challenges.

✔ Start with $500-$1,000 if a full emergency fund feels overwhelming.

✔ Set up automatic transfers to a separate savings account each month.

✔ Avoid using your emergency fund for non-emergencies—keep it strictly for urgent financial needs.

💡 An emergency fund is a financial safety net, giving your family peace of mind. Managing family finances manually can be a headache. Luckily, there are tools to help.

✔ SupportPay – The best way to track shared expenses between co-parents and ensure child-related costs are split fairly.

✔ Mint – Budgeting and expense tracking.

✔ Personal Capital – Long-term financial planning and investment tracking.

💡 Financial tools make planning easier by automating budgeting, payments and tracking – all while keeping records accessible.

**3. Family Financial Planning for Different Situations

Every family is unique. Here’s how financial planning looks for different types of families:

For Co-Parents:

✔ Keep child-related expenses fair and documented with SupportPay.

✔ Communicate openly about big financial decisions.

✔ Set clear expectations for who pays what.

For Single Parents:

✔ Focus on building an emergency fund as a safety net.

✔ Apply for scholarships, grants and tax credits to ease the burden.

✔ Plan for long-term financial independence with investments.

For Blended Families:

✔ Consolidate expenses and create a joint budget with your partner.

✔ **Decide what to do with existing debts or child support payments.

✔ Use financial transparency tools to track expenses across multiple households.

A Financial Plan = A Stronger Family

Creating a financial plan can seem daunting, but taking small, intentional steps makes all the difference.

✔ Assess your financial situation

✔ Set short- and long-term goals

✔ Follow a budget that works for your family

✔ Build an emergency fund for peace of mind

✔ Use SupportPay to manage shared expenses easily

💡 The best financial Plan is the one you stick to. Start today and give your family the financial stability it deserves.